We dig deeper than vague tweets and politically motivated leaks to provide our thoughts on what the impact the Trade War means for investors, and most importantly the opportunities that will emerge.

Is anyone else getting sick of how much attention the Trade War rhetoric is receiving? We certainly are.

However, with China contributing nearly half of total global growth and continued confidence required to sustain American consumer spending and business investment, the broader implications of this ongoing spat go well beyond the products impacted directly by tariffs.

Over the last few months we have travelled throughout the US, Europe, China and other parts of Asia meeting with companies from a range of different sectors. We have been keenly listening to what actual businesses have been telling us about the impact that the Trade War is having on them. In this note we seek to dig deeper than vague tweets and politically motivated leaks and provide our thoughts on what this all means for investors and most importantly the opportunities that will emerge.

But first, we focus on what really lies behind all of this.

The politics of Trump and curbing China’s growth

Let’s make one point clear. No jobs are heading back to the United States, but they are not staying in China either.

Several US-based companies we’ve spoken to have either finished or are close to finishing a transfer of production facilities out of China into other low cost countries like the Philippines, Malaysia, Vietnam and India. We met a US-based manufacture of TV remotes that commented “while it was a painful move, our new factory in the Philippines will improve group margins by 200 basis points and we wish we had moved two years ago.”

We have met apparel retailers that are no longer making belts and handbags in China and a climbing equipment company that is no longer manufacturing carabineers in the Far East. All of these production transitions were put in motion nearly a year ago, and most importantly: no one seems too concerned about the loss of their Chinese manufacturing base.

It begs the question: if the tariffs have set in motion a meaningful shift of low-value manufacturing out of China, does China care? And if not, what is the United States trying to accomplish through tariffs?

The reality is the US is not after low cost jobs out of China, and China knows these jobs are not its future either. Politics, as usual, are rebranding these decisions. President Trump sees “Hard on China” as his best political capital in front of the 2020 elections. China’s retaliatory tariffs directly target Trump voters (no coincidence that Kentucky bourbon and pork are now subject to heavy tariffs).

So the President is branding the trade war as an attempt to protect his constituents by turning the tide on employment outflow, while China is trying to tax his voter base. But the near-term “tit for tat” is just a charade, and pales in comparison to the long-term implications of this standoff. What is really at stake? Intellectual property, forced technology transfer and China’s push to be a new and improved global super power.

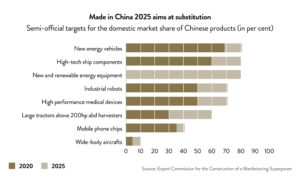

The US is hoping to slow China’s transition to a high value add economy. Tariffs focused on high value industries like technology and aerospace are designed to blunt demand from one of China’s largest end markets. The ban of Huawei 5G technology likely has as much to do with public security as protecting private enterprises. Overall, the hope is to limit the innovation curve clearly targeted by the Made in China 2025 plan.

But has the horse already bolted?

China is aware it’s no longer the low cost labor force for the world, with manufacturing labor costs having risen 15% p.a. since 2000, they have been focused on moving up the value-add chain for several years. When China entered the WTO in 2001, US factories were 14x more productive. This has now halved and continues to narrow. In 2011, the US has 3x the robots in manufacturing plants than China, now the majority of China’s higher value factories operate on a similar standard.

Two machine vision companies we met last week in Germany explained this evolution. They have been supplying Chinese factories for the past few years, putting quality control scanners at the end of production lines where the majority of the lines are still operated by relatively low cost labor. As one company aptly stated, “you can’t monitor manual labor with machine vision”. So the virtuous circle works as such: replace labor with automation, monitor automation with machine vision, use machine vision to optimize production, automate further. Repeat.

We have seen this first-hand in Germany with the world’s leading producer of hydro pneumatic devices to the automotive industry (layman’s term: the spring that helps smoothly open the boot of your car). The majority of the world’s gas springs are manufactured on a compact factory floor full of robots, machine vision devices and only two manual laborers.

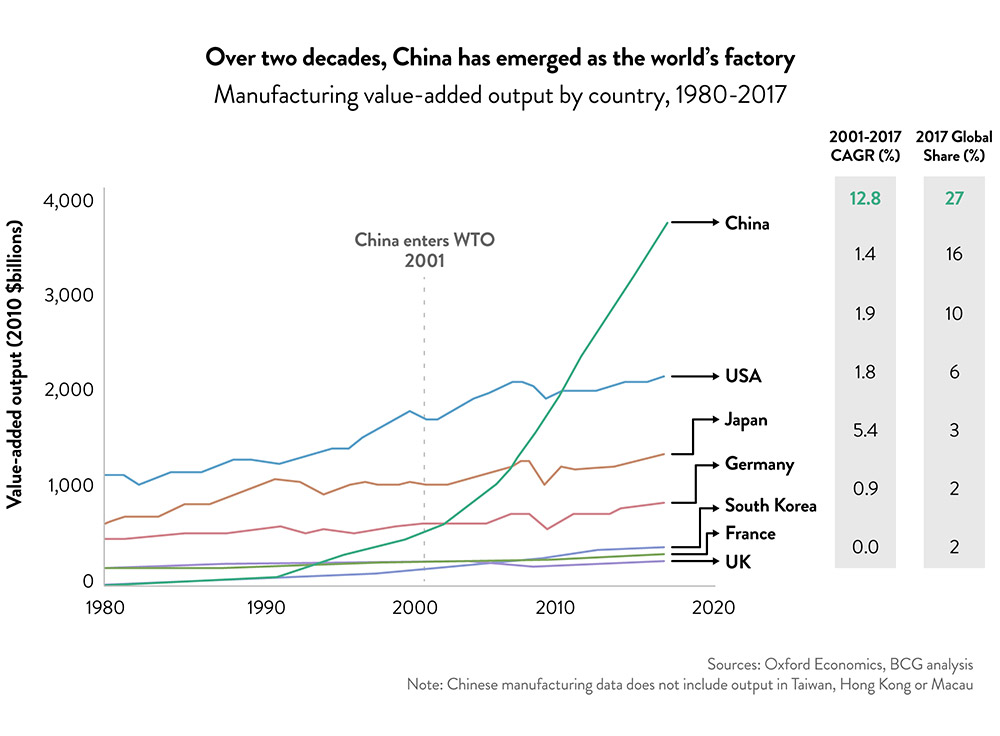

China already generates more real value-add in its factories than US, Germany, UK and South Korea combined, giving it immense scale coupled with a rapidly sophisticated domestic market. We think it is likely past the point where the US can stop its evolution into a high value add, innovation driven economy. Indeed, Chinese patent applications have increased 4x since 2011 to 1.2 million a year.

The US Chamber of Commerce released a relatively scathing review of the made in China 2025 policy in early 2017 where it highlighted the threat of the plan to the US economy and the unlikely benefit to US businesses due to the high internalization targets and limited free market behavior.

What does this mean for us as investors?

Clearly the Tariff War headlines are focused on the risks: lower global growth, increased nationalism of trade and potential destabilization of global economies. Like all investors, at Ophir we are closely monitoring the Trade War so that we avoid those sectors which are most exposed in the short to medium term.

However, we are also focused on looking through the obvious risks to identify how we position our portfolios to steer clear of longer term pitfalls and take advantage of the investment opportunities which will emerge from this accelerating battle for innovation. Our current thinking is guided by three key insights:

- Firstly, Australian investors during the last decade profited from Chinese companies buying up Australian resource companies. With China moving up the value-chain we don’t expect that these ‘free kicks’ will be handed out as readily in the future. We expect that returns will be harder sought but could be much more rewarding as true defendable success in the China market can deliver outsized returns for several years rather than short-term M&A premiums.

- Secondly, with Chinese companies increasingly focused on automation and digitization, opportunities in machine vision, factory automation and the Internet of Things will emerge. Companies that are exposed to these themes will benefit from structural growth tailwinds and we continue to search for opportunities in the Australian market, although currently these opportunities are limited.

- Finally, as the innovation race heats up Chinese companies will naturally seek to leverage the intellectual property of other companies to fuel their development and growth. We recently met two separate Chinese companies who referenced their JVs with international partners were enabling them to learn the processes internally before scaling down the JV, commenting this is a reality in China. As a result, Australian companies that compete on the global stage and flourish will be those with true intellectual property (think IEL) or defensible brands (think A2 Milk).